The Operating Cash Flow Mismatch: Earnings Manipulation Revealed by Cash Flow

Thus began the unraveling of a financial illusion — a classic mismatch between reported profits and operating cash flow. On the surface, the company appeared prosperous. But a closer examination of the cash flow statement revealed something very different.

“Paper profits are easily conjured. Real cash is harder to fake.”

The Illusion of Earnings

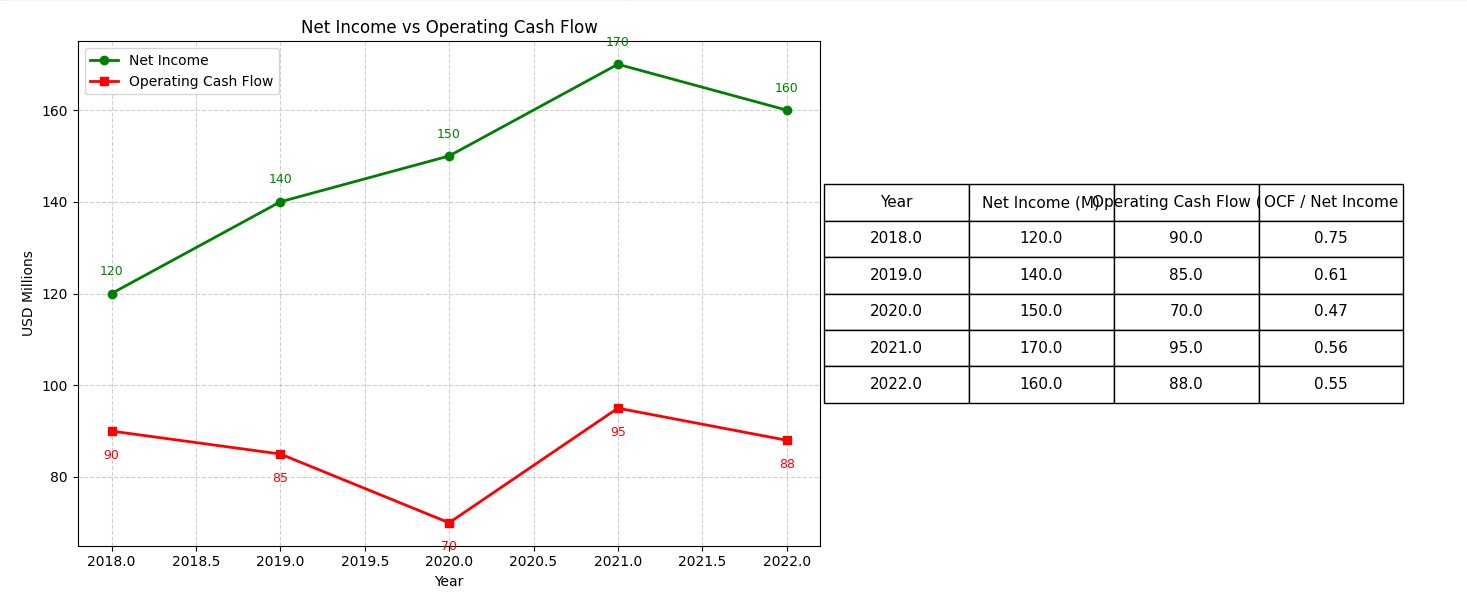

Companies can use accounting adjustments, aggressive accruals, or revenue recognition tactics to inflate their earnings. But the operating cash flow (OCF) statement often tells a more grounded truth. It strips away accounting fiction and reveals whether a company’s operations are truly bringing in cash.

Global Case References

| Company | Year | Reported Net Income | Operating Cash Flow | Red Flag |

|---|---|---|---|---|

| Valeant Pharmaceuticals | 2015 | $73M | -$163M | Channel stuffing, deferred payments |

| WeWork | 2018 | $1.9B Loss | -$1.5B | Non-cash marketing & soft expenses |

| Hyflux | 2017 | $62M | -$97M | Advance revenue, working capital drain |

Forensic Tool: OCF-to-Net Income Ratio

OCF-to-Net Income = Operating Cash Flow / Net Income

A healthy company typically shows an OCF-to-Net Income ratio close to 1 or greater. A persistently low or negative ratio suggests the profits may be overstated or non-cash in nature.

Common Mismatches Between Earnings and Cash Flow

| Red Flag | Accounting Appearance | Cash Reality |

|---|---|---|

| Channel Stuffing | Strong sales growth | Uncollected receivables |

| Capitalized Expenses | Improved margins | Cash outflow classified as capex |

| Deferred Revenue Recognition | Revenue upfront | Cash delayed or prepaid |

Detective’s Note 🕵️

- Always compare net income to operating cash flow. Discrepancies can signal aggressive accounting.

- Check for unusual working capital movements — rising receivables or falling payables.

- Analyze the OCF-to-Net Income ratio over multiple years to catch patterns.

- Cash is hard to fake. Start your investigation there.

more mysterious financial statements.

“There is nothing more deceptive than an obvious fact.” – Sherlock Holmes