🕵️ The Interest Payment Illusion: How Companies Juggle Debt Servicing

“Watson,” Holmes whispered, glancing over a glossy annual report, “this firm pays interest without ever truly earning it.”

“Is that even possible?” I asked.

“Quite. In fact, it’s rather fashionable in the age of cheap debt and clever accounting.”

In the foggy alleys of corporate finance, some companies boast strong EBITDA and proud profitability — while quietly siphoning cash just to service interest payments. This is the illusion: debt appears manageable, but beneath the surface, operations barely generate enough to cover the cost of capital.

🔎 The Case of the Juggled Journal

Our suspect? A listed infrastructure firm with multi-decade debt, high dividends, and stagnant operating cash flows. While its income statement looked healthy, Holmes noted inconsistencies in its financing section:

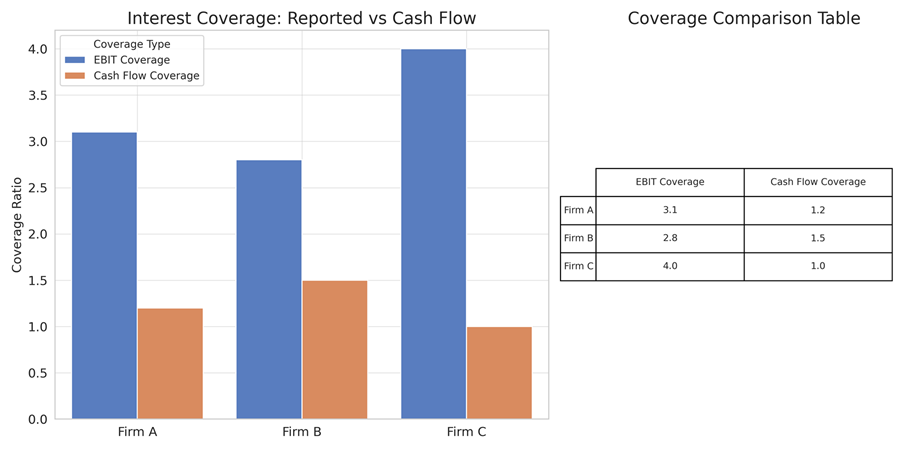

- Net income covered interest 3x — but operating cash flow barely did so 1.2x

- Year-over-year cash interest paid rose 18%

- They issued bonds to pay prior interest — not principal

📉 Interest Coverage Discrepancy Table

| Metric | Reported | Cash Reality |

|---|---|---|

| Interest Coverage Ratio | 3.1x (EBIT basis) | 1.2x (Operating Cash Flow basis) |

| Interest Paid | $120M | Funded $60M via bond issuance |

📊 Interest Coverage vs Debt-to-Equity — A Leverage Trap Unveiled

🚩 Red Flags in Interest Management

- Consistently lower interest coverage on cash basis

- New debt issued frequently with minimal principal reduction

- Rising debt service costs despite flat earnings

- “Adjusted EBITDA” excludes key interest and capex adjustments

📜 Detective’s Note

When companies stretch debt to fund interest — not growth — they trade stability for illusion. Interest expense is not just a line item, it’s a litmus test of financial integrity. Watch the cash, not the clever narrative.

“The most deadly debts are those that hide in plain sight.” – Sherlock Holmes

more mysterious financial statements.