🕵️ The Hidden Liability Case: Uncovering Off-Balance-Sheet Debts

The lamp flickered above us as Holmes stared at the client’s ledger — or rather, what was missing from it.

“Watson,” he said without looking up, “this company is as light on paper as a magician’s trick. What we need to find is what’s not there.”

“You mean liabilities?” I asked.

“Precisely. Debts hidden just out of sight — buried in subsidiaries, partnerships, or worse, in language.”

In the world of finance, what isn’t disclosed can be more revealing than what is. The case of hidden liabilities — debts kept off the balance sheet — is one of the most common yet subtle deceptions in corporate reporting. From leasing games to cleverly worded guarantees, these liabilities haunt the footnotes and threaten investors with unseen risk.

🔍 Smoke, Mirrors, and the Debt That Isn’t There

The firm in question, a global logistics operator, showed pristine financials. Low debt-to-equity. High ROCE. But when Holmes examined their contract disclosures, he raised an eyebrow. A string of complex service agreements with embedded guarantees revealed a web of obligations — none of which appeared on the balance sheet.

- Long-term lease obligations buried in footnotes, not capitalized

- Guarantees issued to finance JV partners, unrecorded as liabilities

- Special purpose vehicles (SPVs) carrying major debt, not consolidated

“The cleanest balance sheet may simply be the most carefully scrubbed.”

📜 Classic Off-Balance-Sheet Mechanisms

| Mechanism | What It Looks Like | What It Really Means |

|---|---|---|

| Operating Leases | Rental payments, not asset ownership | Long-term obligations disguised as expenses |

| SPVs or Affiliates | \”Independent\” financing vehicles | Debt vehicles often guaranteed by parent |

| Guarantees or Put Options | Rarely quantified in the main statements | Potential liabilities triggered under pressure |

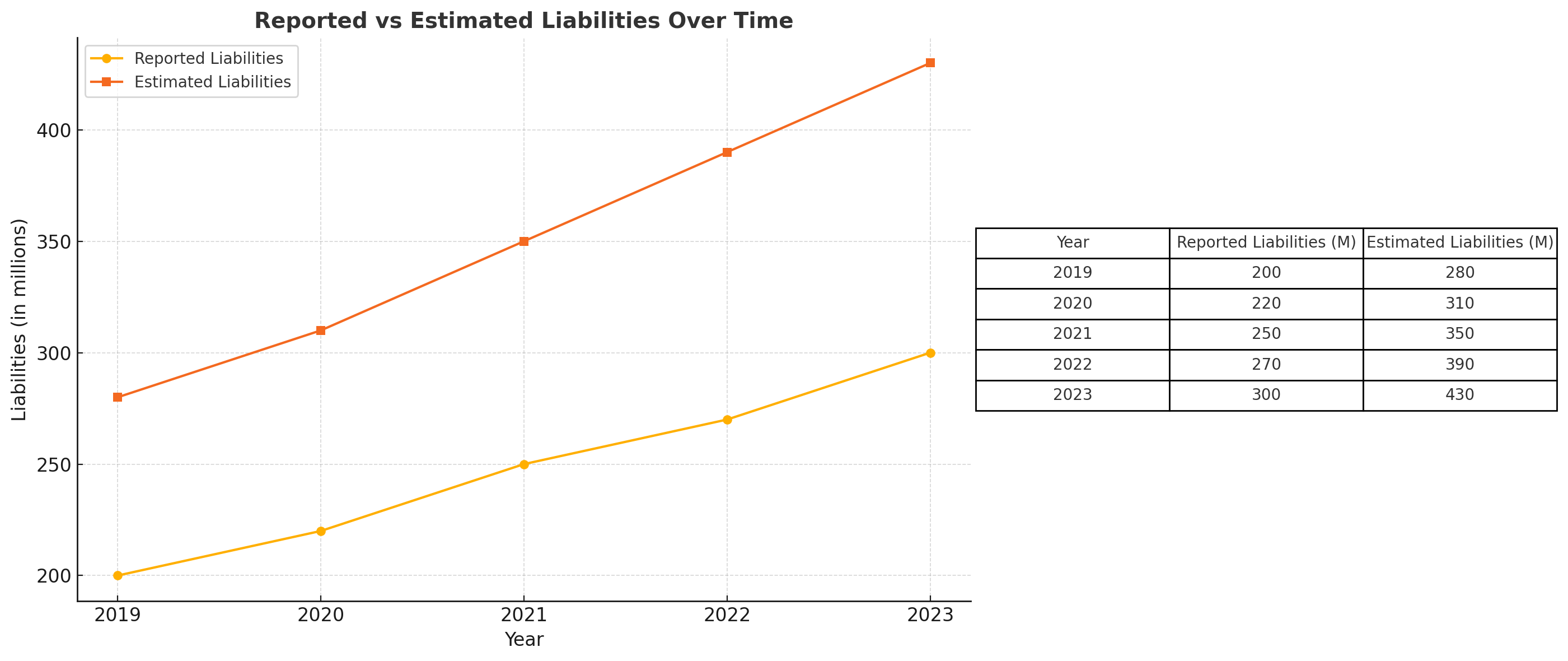

📊 Visualization: Reported Debt vs Actual Obligations

A forensic chart comparing reported liabilities versus adjusted obligations reveals the full risk exposure.

📁 Real-Life Case Reference: Hyflux (Singapore)

Hyflux, a Singaporean water treatment firm, touted asset-light infrastructure and lean financing. In reality, it had complex obligations via preference shares, perpetual securities, and off-balance sheet project debt. When the illusion cracked, it defaulted spectacularly, wiping out thousands of retail investors.

🚨 Red Flags for Hidden Debt

- Footnotes with vague language around guarantees or leases

- Large difference between EBITDA and Operating Cash Flow

- High off-balance-sheet assets but low reported debt

- Presence of unconsolidated JVs or SPVs

- Discrepancies between credit ratings and leverage ratios

📜 Detective’s Note

The greatest risk isn’t always in what’s declared — but in what’s deferred, disguised, or simply left out. Off-balance-sheet debt is the accountant’s equivalent of a trapdoor. A financial sleuth must dig into the footnotes, analyze lease structures, probe affiliate arrangements, and always, always reconcile economic substance with reported form.

“There is nothing more deceptive than an obvious fact.” – Sherlock Holmes

more mysterious financial statements.