The Current Ratio Riddle:The Dark Side of High Ratios

“Watson, do you see this company’s current ratio?” Holmes asked, raising an eyebrow.

“A remarkable 4.5! Surely that’s a mark of strength,” I replied.

Holmes smiled knowingly. “Or a sign they’re hoarding assets they can’t convert — a fortress built of sandbags, not stone.”

At first glance, a **high Current Ratio** is toasted by investors and analysts alike — a beacon of strong liquidity, suggesting that a company can easily cover its short-term obligations. After all, who wouldn’t prefer a surplus of assets over looming liabilities?

Yet, as Sherlock Holmes would caution, “It is a capital mistake to confuse abundance with efficiency.” A **Current Ratio** soaring far above industry norms — say beyond 3.0 or 4.0 — may whisper of deeper issues:

- Idle Assets: Excessive cash or inventory sitting unutilized, earning nothing, while opportunities pass by.

- Poor Working Capital Management: The company may be hoarding current assets due to uncertainty or operational inefficiencies.

- Struggling to Invest: A reluctance or inability to deploy resources into growth-driving initiatives.

- Distress in Disguise: In some cases, suppliers may have tightened credit, forcing companies to stockpile liquid assets as a defensive measure.

Figure: A high Current Ratio isn’t always a sign of strength — it can reveal inefficiency and hidden risks.

Therefore, while a **healthy Current Ratio** (typically between 1.5 and 2.5 depending on industry) reflects sound liquidity, an excessively high figure could be a red flag — not of impending insolvency, but of **missed opportunities and inefficiency**.

\”Watson, even a surplus can signal trouble if it’s merely unused potential gathering dust.\” – Sherlock Holmes

🔎 The Case of Excessive Cushion

A manufacturing firm reported a stellar current ratio of 4.5. Yet Holmes noticed:

- Bloated cash reserves due to delayed investments

- Receivables aging beyond 120 days

- Inventory piled up from canceled orders

🔎 The Current Ratio Riddle: The Case of Excessive Cushion

On paper, the manufacturing firm appeared to be a paragon of liquidity — boasting a **Current Ratio** of 4.5. To the untrained eye, it was a fortress of financial stability. But as Holmes would say, “The larger the cushion, Watson, the more one must ask — what fall are they expecting?”

A deeper forensic examination revealed that this so-called “excess cushion” was less a sign of prudence and more a silent alarm of operational stagnation:

- Bloated Cash Reserves: The firm had accumulated significant cash, not from strategic foresight, but due to repeatedly postponed capital investments. Projects intended to drive growth were shelved amidst management indecision, leaving funds idle — a missed opportunity in disguise.

- Receivables Aging Beyond 120 Days: A closer look at the accounts receivable ledger showed a worrying trend — customers delaying payments well past standard terms. What appeared as ‘current assets’ were, in reality, fading promises of cash, hinting at weakening credit control and potential bad debts lurking.

- Inventory Piled Up from Canceled Orders: Warehouses were brimming, not in anticipation of demand, but due to canceled contracts and forecasting errors. Each unsold unit silently eroded value through storage costs, obsolescence risk, and capital lock-up.

What seemed like a healthy buffer was, in truth, a tapestry of inefficiencies and deferred problems. The company wasn’t fortified — it was immobilized.

\”Watson, when a company builds walls too thick, it often traps itself within.\” – Sherlock Holmes

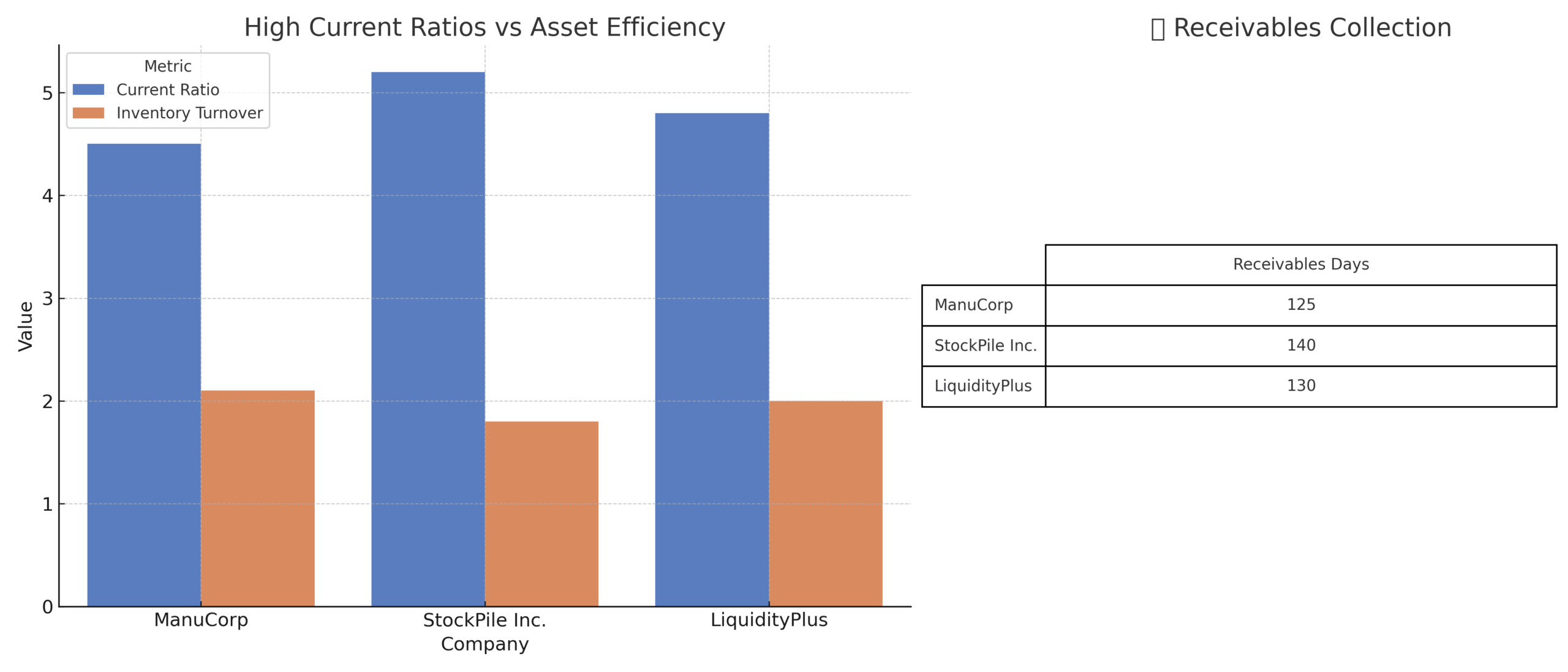

📉 Asset Efficiency Snapshot

| Metric | Value | Forensic Insight |

|---|---|---|

| Current Ratio | 4.5 | Liquidity surplus masking inefficiency |

| Receivables Days | 125 days | Potential collection issues |

| Inventory Turnover | 2.1x | Excess stock from weak demand |

🚩 Red Flags Behind a “Healthy” Current Ratio

A robust Current Ratio often earns applause in boardrooms and balance sheet reviews. Yet, as any forensic detective of finance would attest, numbers can be master illusionists. Beneath the surface of a seemingly “healthy” liquidity metric, subtle warnings often lurk — easily missed by those who admire the façade but fail to inspect the foundation.

- Unusually High Cash Balances Without Strategic Deployment:

While cash is king, an idle monarch serves no kingdom. Excessive cash reserves, when not earmarked for investment, debt reduction, or strategic initiatives, suggest either a lack of vision or fear-driven hoarding. In a thriving enterprise, cash should be working — funding growth, innovation, or shareholder returns. Piles of dormant cash may indicate management paralysis or anticipation of stormy weather ahead.

- Unusually High Cash Balances Without Strategic Deployment:

- Slow Receivables Collection Cycles:

A ballooning accounts receivable figure can deceptively boost the current ratio. But when customers stretch payments beyond agreed terms, it signals weakening credit control or desperate sales tactics (extending lenient terms to secure deals). The longer the collection cycle, the higher the risk that these “assets” transform into bad debts. Healthy liquidity cannot stand on promises that age poorly.

- Slow Receivables Collection Cycles:

- Inventory Buildup Signaling Demand Issues:

Warehouses filled to the brim may look like preparedness, but often they whisper of a darker tale — misjudged demand, canceled orders, or inefficient production cycles. Inventory is only as valuable as its ability to convert into cash flow. Prolonged stockpiles lead to obsolescence, increased holding costs, and tied-up capital — turning what appears as an asset into a slow-moving liability.

- Inventory Buildup Signaling Demand Issues:

- Deferred Liabilities Creating a False Sense of Security:

Some firms negotiate extended payment terms with suppliers or delay recognizing certain obligations, artificially lowering current liabilities. While this flatters the current ratio, it’s akin to sweeping dust under the carpet — the obligation remains, merely postponed. Such practices may hint at cash flow pressures or aggressive accounting tactics designed to present a rosier liquidity picture.

As Holmes would advise, “It is not enough to observe the number, Watson — one must question what gives it shape.” A towering current ratio, when built on fragile foundations, is less a sign of strength and more a silent plea for attention.

📜 Detective’s Note

Liquidity should be balanced — too low invites risk, too high hints at stagnation. Always question why a company is holding excessive current assets and whether it reflects strategy or symptoms.

“Watson, even a surplus can signal trouble if it’s merely unused potential gathering dust.” – Sherlock Holmes

more mysterious financial statements.