The Current Ratio Conundrum: When Liquidity Ratios Give False Comfort

And just like that, we were off — investigating yet another case of a healthy-looking balance sheet that hid ailing internals. The current ratio, often cited as a beacon of short-term solvency, can mislead even seasoned analysts if they fail to examine what’s beneath those ‘current’ labels.

“Liquidity, Watson, is not about what’s listed — it’s about what’s liquid.”

The Illusion of Coverage

The current ratio is a blunt instrument. It simply divides current assets by current liabilities. But what if the assets include slow-moving inventory, doubtful receivables, or restricted cash? Suddenly, the so-called liquidity becomes as misleading as a forged alibi.

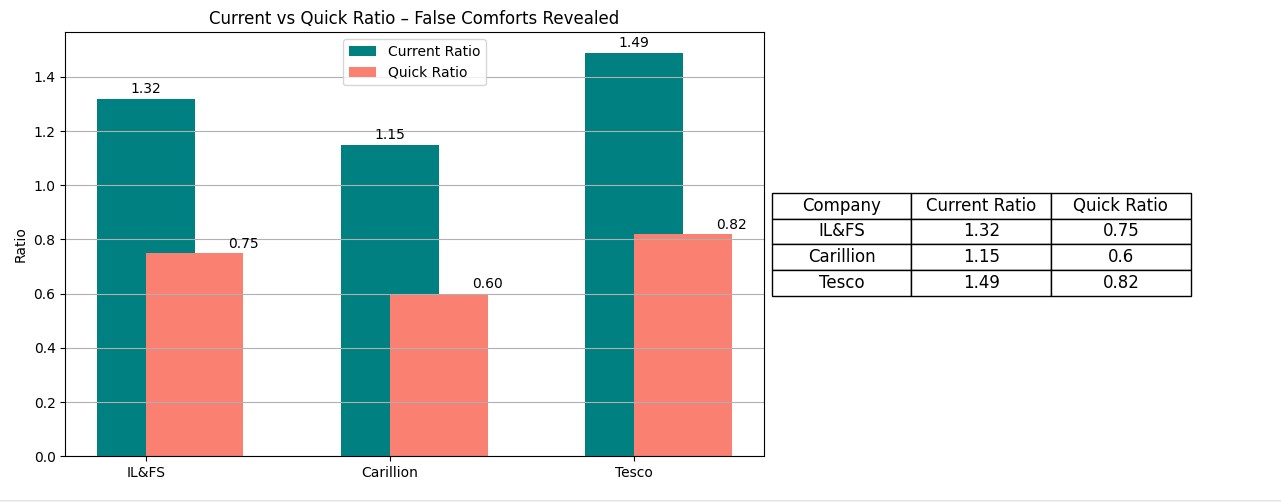

Case Studies of Misleading Liquidity

| Company | Region | Reported Current Ratio | Red Flag | Real Problem |

|---|---|---|---|---|

| IL&FS | India | 1.32 | Inflated receivables | Cash crunch and default |

| Carillion | UK | 1.15 | Inventory valuation manipulation | Insolvency within months |

| Tesco | UK | 1.49 | Trade payable timing tricks | Overstated profits and restatement |

Forensic Tool: Quick Ratio (Acid Test)

Quick Ratio = (Current Assets – Inventory – Prepaids) / Current Liabilities

This more stringent version removes the fluff. If a company has a high current ratio but a weak quick ratio, we start investigating what’s clogging the short-term pipes.

Visual Clue: Current vs Quick Ratio

Tricks That Distort the Ratio

| Tactic | How It Looks | What’s Really Happening |

|---|---|---|

| Channel Stuffing | High receivables | Unsold goods parked with distributors |

| Inventory Reclassification | Healthy current asset line | Obsolete stock at full value |

| Deferred Payables | Lower current liabilities | Shifted debt to future periods |

Global Red Flags to Watch

- Hyflux (Singapore): Reported strong liquidity while struggling to pay suppliers

- SunEdison (US): Boasted a healthy current ratio pre-bankruptcy

- Gitanjali Gems (India): Inflated inventory and fake receivables to mask liquidity gaps

Detective’s Note 🕵️

- Current ratios can be cosmetic. Always compare them with the quick ratio and cash flow health.

- Review inventory and receivables aging schedules for signs of impairment.

- Check notes for restricted cash, channel stuffing, or deferred payables.

- Liquidity is not about labels. It’s about what can be converted into cash — and when.

“It is a capital mistake to theorize before one has data. Insensibly one begins to twist facts to suit theories.” – Sherlock Holmes