The Case of Negative Cash Flow: Why Profitability Doesn’t Always Mean Liquidity

Thus began our journey into the curious world of companies that appear profitable — yet are gasping for liquidity. The mismatch between net income and actual cash flow is one of the oldest sleights-of-hand in finance, and one of the most dangerous.

“The balance sheet can smile, Watson, while the cash register weeps.”

Profit vs Cash Flow: A False Equivalence

Accrual accounting allows revenues to be booked before they’re paid, and expenses to be delayed. This creates a dangerous illusion: a business that’s ‘profitable’ on paper but losing oxygen in reality. Negative operating cash flow, even in the presence of net profit, is the ultimate red flag.

Real-World Cases of Profitable Loss

| Company | Year | Net Profit | Operating Cash Flow | Red Flag |

|---|---|---|---|---|

| Jet Airways (India) | 2017 | $160M | -$220M | Revenue recognition outpaced cash receipts |

| WeWork | 2018 | $1.9B Loss | -$1.5B | Non-cash adjustments, aggressive expansion |

| Valeant Pharmaceuticals | 2015 | $73M | -$163M | Delayed receivables, channel stuffing |

Forensic Tool: Operating Cash Flow Margin

OCF Margin = Operating Cash Flow / Revenue

If this margin is consistently negative while net income remains positive, there’s a serious disconnect between what a company says it earns — and what it actually collects.

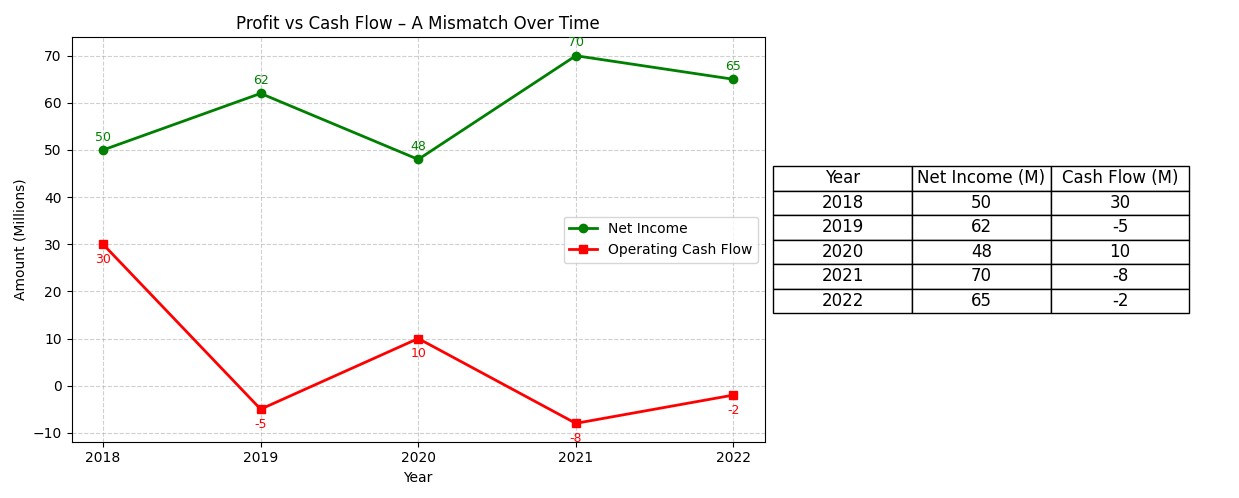

Net Income vs Operating Cash Flow

Classic Tricks Behind the Discrepancy

| Tactic | What It Looks Like | The Reality |

|---|---|---|

| Channel Stuffing | Surging sales in Q4 | Inventory pushed to distributors, unpaid |

| Capitalized Costs | Lower expenses, higher profits | Cash spent but deferred from P&L |

| Revenue Recognition Loopholes | Contracts booked upfront | Cash spread over months or years |

Red Flags in the Wild

- Startups: Frequently show growth and losses, but also negative cash flow — burning capital

- Real Estate Developers: Recognize revenue on project progress, but cash may be years away

- Retail Chains: Deep discounting and overstocking inflate sales without real liquidity

Detective’s Note 🕵️

- Always reconcile cash flow with net income. Look for major non-cash adjustments.

- Compare revenue growth with OCF trends — they should generally move together.

- Check working capital movement: rising receivables and inventories may explain the gap.

- Negative cash flow is forgivable in investment-heavy phases — but not indefinitely.

“Data, data, data! I can’t make bricks without clay.” – Sherlock Holmes