The Corporate Debt Avalanche

This article is not just a story — it is an investigation. Through a Sherlock Holmes-inspired narrative, we explore how corporate debt, once hailed as a strategic lever, can quietly become a systemic risk. What follows blends fiction and financial reality to help you spot danger long before the collapse.

Before we unravel the clues, let us first examine the ledger.

The following sections chart the path of inquiry — from the first crack to the final reckoning.

| 📚 Table of Contents | |

|---|---|

| A Most Unusual Collapse | The fictional case of Gallowmere Industries — a chilling prelude to the corporate debt storm. |

| The Sweet Seduction of Cheap Debt | How a decade of low interest rates lured companies into risky financial decisions. |

| The Avalanche Begins | Early warning signs: shrinking interest coverage, looming maturities, and covenant breaches. |

| Real Cases from the Ledger | 🔎 Evergrande — The Colossus on Crumbling Foundations |

| 🔎 Altice — Growth by Debt, Unwinding by Reality | |

| 🔎 WeWork — Leases Masquerading as Stability | |

| ✅ Ford — The Unexpected Survivor | |

| Footnotes Never Lie | Hidden debt, ballooning leases, and dangerous assumptions buried in financial fine print. |

| The Avalanche Roars | Downgrades, defaults, fire sales, and the widening cracks across markets and industries. |

| Detective’s Note — Key Takeaways | Five forensic lessons from Holmes on debt, timing, and financial resilience. |

| Closing Sherlock Quote | A final warning — written in smoke and silence. |

A Most Unusual Collapse

(The following is a fictional scene, inspired by the investigative spirit of Sherlock Holmes, crafted to illustrate real-world financial dynamics.)

It was a bitter evening in late November, the sort that persuades even the Thames to shiver beneath its fog. I had just settled into my armchair with the Financial Times when Holmes, pacing about 221B like a hound denied the hunt, suddenly halted at the mantelpiece.

He held in his hand an envelope, aged but unopened, stamped with the insignia of a well-known conglomerate.

“Watson,” he said sharply, “do you recall the case of Gallowmere Industries?”

“Of course,” I replied. “Darling of the stock exchange. ‘Bulletproof balance sheet,’ the analysts claimed.”

Holmes smirked. “Yes, until this morning.”

With a flick, he opened the report. The scent of varnished deceit wafted out as if the ink itself had tried to hide something. Holmes laid it across the table like an autopsy.

Figure: Rising Net Interest Expense Hidden Beneath Non-Operating Gains

“Observe page 74. Note the subtle rise in net interest expense — masked by non-operating gains. Quite the sleight of hand.”

I leaned over. “But they posted record EBITDA. Surely that counts for something?”

“EBITDA, my dear Watson,” Holmes said with a grim smile, “is the most accommodating of guests — it lets debt sit at the table without asking how it got there.”

He drew a circle around a footnote at the bottom.

“‘Refinancing expected to be routine,’” he read aloud. “There lies the body buried — they built their empire on rolling short-term debt in a rising-rate world.”

“And now?”

“They missed a bond payment yesterday. Creditors are circling. This, Watson, is not a company in decline. It’s a company that mistook leverage for growth — and now stands at the very brink of The Corporate Debt Avalanche.”

The lamplight flickered. Somewhere, a carriage rattled past Baker Street, unaware that in a quiet room above, two men had just uncovered the opening tremor of a corporate reckoning.

The Sweet Seduction of Cheap Debt

The next morning, over a breakfast of strong coffee and weaker crumpets, Holmes unfurled a collection of balance sheets across our dining table as though arranging pieces on a chessboard.

“Understand this, Watson,” he began, tapping a ledger emphatically, “the seeds of The Corporate Debt Avalanche were not sown in panic, but in euphoria.”

I raised an eyebrow. “How so?”

Holmes leaned back, steepling his fingers in thought.

“For over a decade, the world lived under the intoxicating spell of cheap money. Central banks, eager to revive sluggish economies, flooded the markets with liquidity. Interest rates plunged to historic lows. Debt, once a solemn contract, became an afterthought.”

He flipped open a glossy investor presentation.

“Companies, large and small, could borrow at will — not to survive, but to expand recklessly, to buy back shares, to acquire rivals at fantastical valuations. Growth was no longer funded by grit or ingenuity, but by leverage.”

“And the investors?” I asked.

Holmes allowed himself a dry chuckle. “They cheered it, Watson. Each bond offering, each leveraged buyout, each share repurchase sent stock prices soaring. The very structure of reward became skewed — caution was punished, risk was lionized.”

He pointed to a familiar ratio scribbled in the margins: Debt-to-EBITDA.

“As debt mounted, financial metrics grew distorted. Earnings looked robust on the surface, yet the scaffolding beneath was increasingly brittle.”

A cold draft slipped in through the cracked window, stirring the papers like restless ghosts.

“Thus,” Holmes concluded, “while the world toasted its own cleverness, it unknowingly laid the foundation for what we now recognize as The Corporate Debt Avalanche — a slow, silent accumulation of risk, waiting only for a shift in the weather.”

Outside, the first raindrops tapped against the glass. A storm, it seemed, was brewing both in London’s skies and in its ledgers.

The Avalanche Begins

Holmes wasted no time. By mid-morning, the sitting room at 221B Baker Street resembled a financial war room: ledgers piled high, reports annotated with furious precision, a blackboard scrawled with alarming ratios.

The signs, he noted, had been visible for months — subtle at first, but unmistakable to a trained eye.

🔍 Early Warning Signs of a Corporate Debt Avalanche

| Red Flag | What It Really Means |

|---|---|

| Falling Interest Coverage (<2.5x) | Earnings barely cover interest costs — stress rising. |

| Rapid Growth in Short-Term Debt | Heavy refinancing needed soon — liquidity risk ahead. |

| Covenant Waivers or Silent Amendments | Quiet signs of lender nervousness — financial strain. |

| Negative Operating Cash Flow + Rising Debt | Business model failing to self-fund operations. |

| High Off-Balance-Sheet Lease Obligations | Hidden leverage inflating true liabilities. |

| Overreliance on Refinancing Assumptions | Plans built on hope, not secured funding. |

| Management’s “Strategic Alternatives” Language | Code words hinting at asset sales or distress. |

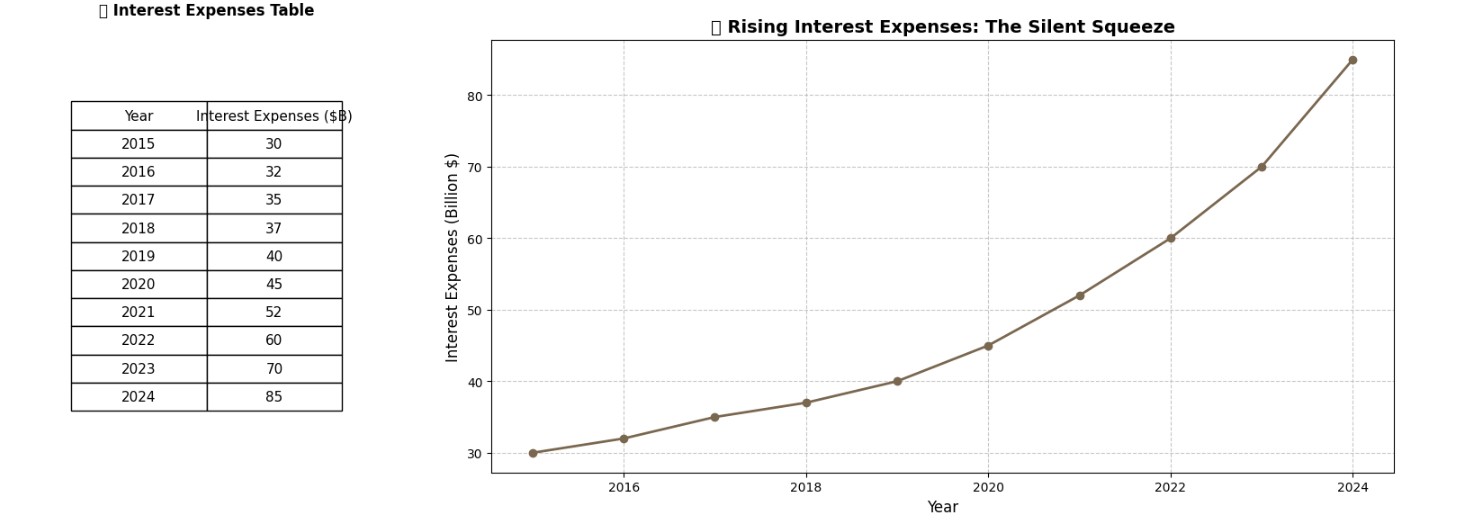

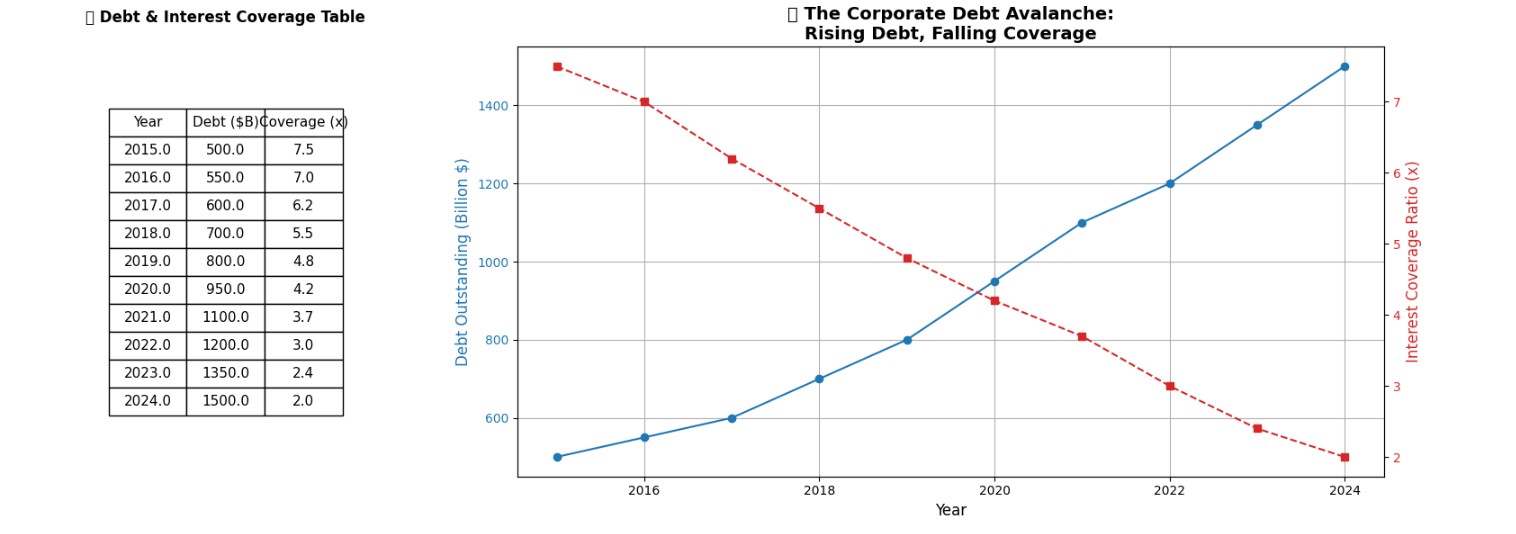

Interest Coverage Ratios Shrinking:

Where once earnings comfortably outpaced interest obligations, now they barely sufficed. A coverage ratio slipping below 2.5 was no longer an anomaly but a pattern, a quiet admission of financial strain.

Figure: Shrinking Interest Coverage in a Rising Rate Environment

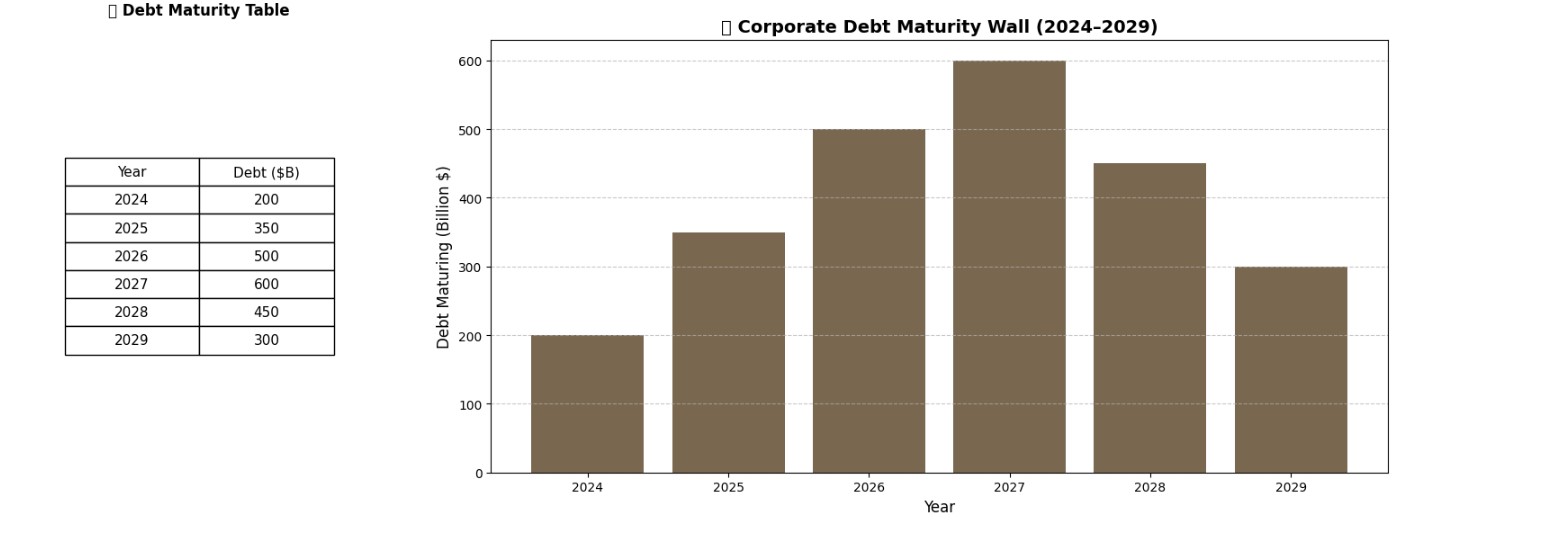

Debt maturity wall Approaching:

Many corporations had layered their debt assuming perpetual access to cheap refinancing. But with borrowing costs rising sharply, the 2025–2027 maturity cliffs loomed like jagged rocks for the overleveraged.

Figure: Corporate Debt Maturities Cluster Around 2025–2027

Negative Operating Cash Flow Coupled with Rising Debt:

Companies that should have been deleveraging post-pandemic instead chose to stack liabilities higher, betting on revenue rebounds that never fully materialized.

Covenant breaches and Silent Renegotiations:

Footnotes in quarterly reports revealed covenant waivers being discreetly sought — a warning shot that lenders were tightening the noose.

The most dangerous part of an avalanche, Holmes observed, is not the initial crack. It is the false sense of calm that follows, moments before the mass descends.

So it was with corporations.

Balance sheets still looked presentable.

Earnings guidance remained upbeat.

Yet underneath, the financial equivalent of unstable snowpacks — debt loads swollen against rising rates — grew ever more fragile.

In particular, Holmes flagged three sectors most exposed:

- Real Estate Developers reliant on rolling short-term loans to finance long-term projects.

- Private Equity Portfolios burdened with aggressive leveraged buyouts.

- High-Yield “Zombie” Companies surviving solely by issuing new debt to pay old obligations.

Across earnings calls, a new lexicon was emerging:

- “Temporary dislocation.”

- “Strategic refinancing.”

- “Enhanced capital flexibility.”

All euphemisms, Holmes noted grimly, for firms grappling with the mounting pressure of The Corporate Debt Avalanche.

At this stage, few headlines screamed danger.

But the data whispered it relentlessly — for those, like Holmes, attuned to listen.

Real Cases from the Ledger

As Holmes pored over case files, it became evident that The Corporate Debt Avalanche had already begun claiming its first victims. Their names, once symbols of ambition and dominance, now stood as cautionary tales of leverage abused and liquidity squandered.

🔎 Case 1: Evergrande — The Colossus on Crumbling Foundations

Few stories illustrate the perils of unchecked borrowing better than China’s Evergrande Group. A real estate empire built atop a mountain of short-term debt, Evergrande expanded relentlessly — acquiring land, developing projects, even dabbling in electric vehicles and theme parks.

- Debt exceeding $300 billion, with maturity walls arriving faster than revenue realization.

- Aggressive off-balance-sheet borrowings hidden through structured obligations.

- Cash flows heavily reliant on pre-sales — robbing future revenue to fund today’s promises.

When Chinese regulators tightened funding rules under the “Three Red Lines” policy, Evergrande’s elaborate debt pyramid began to wobble. Payment defaults followed. Projects stalled. Suppliers went unpaid.

What appeared to be a liquidity hiccup revealed itself as insolvency hiding in plain sight.

🔎 Case 2: Altice — Growth by Debt, Unwinding by Reality

Altice, the telecom giant helmed by Patrick Drahi, showcased another breed of overreach. Driven by an insatiable appetite for acquisitions, Altice amassed a sprawling empire funded largely through leveraged debt.

- Debt-to-EBITDA ratios pushing above 5x — alarming even by private equity standards.

- Heavy reliance on refinancing at tight spreads, a luxury that evaporated as interest rates rose.

- Margin pressures from intense competition, squeezing operating cash flows.

As refinancing costs soared and organic growth sputtered, the company’s debt burden — once manageable in a low-rate environment — grew monstrous, forcing asset sales and restructuring efforts.

🔎 Case 3: WeWork — Leases Masquerading as Stability

Not all corporate debt sits neatly on a balance sheet. WeWork, the poster child of flexible office spaces, revealed the dangers of hidden leverage.

- Long-term, fixed-lease obligations worth tens of billions, against short-term, cancellable revenues.

- Aggressive expansion funded by venture capital infusions rather than sustainable cash flow.

- Financial statements that glossed over the time-bomb nature of their lease commitments.

When growth projections faltered and public scrutiny intensified, WeWork’s planned IPO collapsed spectacularly — unveiling a company structurally ill-prepared to service its disguised debts.

🔎 The Unexpected Survivor: Ford Motor Company

Yet, not every highly indebted company succumbed. Ford Motor Company, recognizing the risk early, began deleveraging aggressively post-2020.

- Early repayment of high-interest debt.

- Raising liquidity buffers even at higher cost.

- Shifting capital expenditures toward profitable core segments.

While its journey was not without turbulence, Ford’s proactive steps helped it sidestep the worst impacts of The Corporate Debt Avalanche, proving that foresight remains the most effective antidote.

Thus, Holmes concluded, the real peril was not merely the presence of debt — it was the fragility of the assumptions underpinning it.

Revenue growth, refinancing ease, cheap liquidity — all presumed eternal, yet all inherently mortal.

In the great ledger of corporate finance, it seemed, hubris was paid for in arrears.

Footnotes Never Lie

If the glossy earnings presentations were the polished surface of corporate narratives, the footnotes buried within financial reports were the fissures through which uncomfortable truths seeped.

Holmes, now fully absorbed in his work, attacked the pages of annual reports with a ferocity reserved for the truly guilty.

🔎 Hidden Clues from the Footnotes

📜 Footnote Excerpt 1: Refinancing Assumptions

“The Company anticipates refinancing its $450 million senior notes maturing in June 2025 through future debt issuance or extensions of existing credit lines. Management believes market conditions will remain favorable for such activities.”

🔍 Sherlock’s Commentary: “Observe, Watson — no commitment letters. No backup liquidity plan. Only a hope stitched into the narrative like a hidden tear in the fabric.”

📜 Footnote Excerpt 2: Lease Obligations Hidden Risk

“Operating lease obligations totaling $2.1 billion as of December 31, 2024, are not reflected as liabilities on the consolidated balance sheet, in accordance with applicable accounting standards.”

🔍 Sherlock’s Commentary: “Liabilities, Watson, are like debts whispered behind closed doors. They do not appear at the dinner table — but they arrive for the reckoning all the same.”

📜 Footnote Excerpt 3: Covenant Waiver Obtained

“On October 15, 2024, the Company secured a waiver of its net leverage ratio covenant for the fiscal year ending December 31, 2024, from its senior lenders.”

🔍 Sherlock’s Commentary: “And there, Watson, is the faint scent of panic. A covenant waiver is not a pardon — it is merely a stay of execution.”

Patterns emerged:

🔎 1. Hidden Debt in Joint Ventures and Affiliates

It was a common sleight of hand. By shifting liabilities onto unconsolidated entities — often affiliates where ownership stakes hovered just below regulatory thresholds — companies could reduce their reported debt loads, while maintaining effective control over the obligations.

A footnote might read:

“Entity ABC, a non-consolidated affiliate, holds outstanding obligations of $2.4 billion, non-recourse to the parent.”

Yet operational dependency and reputational risk ensured that when trouble struck, the parent company bore the consequences.

🔎 2. Ballooning Lease Liabilities

New accounting standards had forced companies to recognize operating leases on balance sheets. However, many continued to bury the true scale of these commitments deep within the notes:

- Future lease obligations, stretching 10 to 20 years

- Escalation clauses that grew with inflation indexes

- Minimal right-to-terminate provisions

In aggregate, these off-balance sheet obligations could rival — or even exceed — traditional debt, quietly compounding vulnerability.

🔎 3. Refinancing Assumptions Embedded in MD&A Sections

Management Discussion & Analysis (MD&A) often contained hopeful language:

“Management believes it will be able to refinance upcoming maturities on favorable terms.”

Yet, Holmes noted that many of these assumptions lacked concrete backup:

- No committed credit facilities in place

- Deteriorating credit ratings not disclosed prominently

- Rising cost of capital unaddressed

When optimism masquerades as a financial plan, Holmes mused, disaster is rarely far behind.

🔎 4. Covenant Loosening and Silent Amendments

In times of liquidity, lenders grew complacent — relaxing covenant thresholds for companies teetering on compliance edges.

But as the cycle tightened, those same loose agreements became the weak bridges cracking under stress:

- Waivers quietly obtained — a temporary reprieve, not a solution

- Covenant holidays masking the true deterioration of financial health

Hidden between the lines, these adjustments offered early warnings of companies desperate to avoid tripping alarms.

Thus, Holmes concluded grimly:

“The ledgers may lie, Watson. The press releases certainly do. But footnotes — ah, they confess.”

The sharp-eyed reader could discern the coming tremors of The Corporate Debt Avalanche not from headlines or quarterly calls, but from the fine print others dared not examine too closely.

🧮 Forensic Snapshot: Debt Risk Thresholds

| Metric | Warning Threshold |

|---|---|

| Interest Coverage | < 2.5× |

| Debt-to-EBITDA | > 4× |

| Free Cash Flow | Negative |

| Covenant Waivers | Mentioned in footnotes |

The Avalanche Roars

At first, the failures seemed isolated — distant rumbles easily dismissed by those untrained in listening for echoes.

A mid-sized property developer in China missed a bond payment.

A telecom operator in Europe announced surprise asset sales.

A high-flying tech darling shelved its IPO.

But Holmes, tracing the tremors across markets and continents, recognized the unmistakable pattern: the avalanche had broken loose.

🔴 Credit Rating Downgrades

Investment-grade companies, once considered fortresses, found themselves slipping into high-yield territory — the so-called “fallen angels.”

- Downgrades accelerated.

- Credit spreads widened mercilessly.

- Investor appetite for anything deemed risky evaporated overnight.

In the end, it wasn’t bankruptcy that undid many firms first. It was the slow strangulation of credit access — a world suddenly unwilling to lend, except at ruinous rates.

🔴 Failed Bond Issuances and Fire Sales

Corporations that had planned for routine refinancing now faced a barren marketplace.

- Bond offerings were pulled.

- Debt maturities loomed, unrefinanced and uncompromised.

In desperation, companies turned to asset sales:

- Divisions once deemed “core” were auctioned at discounts.

- Strategic investments were liquidated to raise immediate cash.

- Mergers once touted as synergies dissolved under scrutiny.

Yet, each sale weakened the firm further — stripping future earnings to pay for past mistakes.

🔴 Layoffs, Restructurings, and Reckonings

As liquidity dwindled, operational cuts followed:

- Mass layoffs to preserve cash.

- Restructurings that gutted once-proud enterprises.

- Leadership changes at dizzying pace, as scapegoats were sought.

What began as isolated corporate struggles soon cascaded into broader economic ripples:

- Suppliers left unpaid.

- Projects abandoned mid-construction.

- Pension plans and small investors burned in the fallout.

The Corporate Debt Avalanche spared few. Even firms that entered the crisis with relatively stable footing found themselves battered by the secondary effects — tighter financing conditions, broken supply chains, collapsing customer demand.

🔴 Public Optimism vs Private Panic

Official statements remained stubbornly optimistic:

- “Liquidity position remains strong.”

- “Exploring strategic alternatives.”

- “Focused on long-term value creation.”

But Holmes observed that behind the scenes, the conversations had shifted:

- Emergency board meetings.

- Midnight calls to lenders.

- Secret preparations for bankruptcy filings.

The contrast was stark — the brave public facade versus the private scramble for survival.

Thus, as the avalanche thundered down the financial slopes, it spared neither the careless nor the cautious.

All who had built their fortunes on unstable leverage were now being called to account.

The storm, long foretold in ratios and footnotes, had arrived.

Detective’s Note — Key Takeaways

Holmes closed the final ledger with a soft, deliberate snap. He rose, brushed a speck of dust from his sleeve, and turned to the window, the fog outside as thick as ever.

“You see, Watson,” he said quietly, “the true peril was never the presence of debt. It was the blindness to its compounding dangers.”

The collapse of Gallowmere Industries was not an isolated event. It was merely one face in a far larger reckoning — the slow, inevitable consequence of ignoring basic financial truths.

From the wreckage, Holmes distilled five immutable lessons:

- ✔️ Debt Isn’t Dangerous — Until It’s Unpayable

Borrowing to fund growth is natural. Assuming endless refinancing at cheap rates is fatal. - ✔️ Cheap Money Distorts Judgment

When debt is abundant, poor investments masquerade as brilliant strategies. Only when liquidity recedes does true business quality reveal itself. - ✔️ The Footnotes Hold the First Warnings

Covenant breaches, refinancing assumptions, lease obligations — all whispered of stress long before headlines shouted collapse. - ✔️ Size Offers No Immunity

From startups to empires, leverage respects no hierarchy. Goliaths fall just as surely as minnows when burdened beyond endurance. - ✔️ Resilience Is Built in Good Times, Not in Crisis

Ford’s cautious deleveraging proved one truth few heed: The time to strengthen the balance sheet is not when avalanches loom — it is when the skies are still clear.

Thus concluded Holmes, with that particular glint in his eye reserved for puzzles well unraveled:

“In an era of euphoria, skepticism is the rarest virtue. Yet it is the only one that survives The Corporate Debt Avalanche.”

Closing Sherlock Quote

The lamplight dimmed as Holmes struck a match, lighting his pipe with a contemplative air. Outside, the city rumbled on — oblivious to the silent avalanches reshaping its fortunes.

With a thin smile, he mused aloud:

“The balance sheet, Watson, may look sturdy. But debt, when left unchecked, is the snowflake that triggers the avalanche.”

He tapped the ash from his pipe, the embers briefly flaring — a final warning written in smoke and silence.