The Cash Conversion Cycle Trap: How Slow-Moving Inventory Sinks Cash

The Cash Conversion Cycle (CCC) measures the time it takes for a company to convert its investments in inventory and other resources into cash flows from sales. When this cycle is bloated — especially due to slow-moving inventory — it silently drains working capital, traps cash, and threatens operational stability. In this case file, we trace how the CCC becomes a cunning culprit in financial forensics.

“Cash isn’t lost, Watson. It’s merely imprisoned — in the very goods we failed to move.”

🧮 Understanding the Cycle

The CCC formula is:

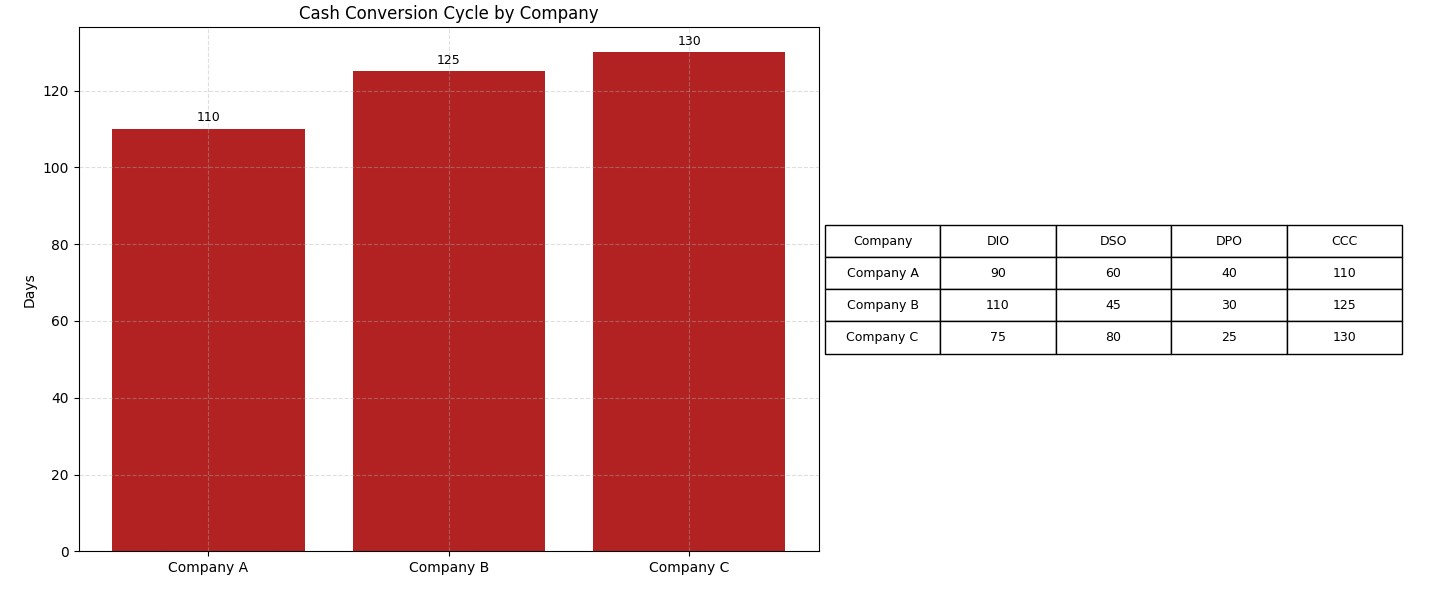

CCC = DIO + DSO – DPO

- DIO (Days Inventory Outstanding): How long inventory is held before it’s sold

- DSO (Days Sales Outstanding): How long it takes to collect cash from customers

- DPO (Days Payable Outstanding): How long the company takes to pay suppliers

A high CCC means the company’s cash is tied up longer — increasing working capital needs, funding gaps, and even borrowing costs.

🏭 Real-World Examples

| Company | Issue | Red Flag | Impact |

|---|---|---|---|

| Forever 21 | Excess inventory from expansion | High DIO, low turnover | Cash drain led to bankruptcy |

| JCPenney | Slow-moving seasonal goods | Rising CCC year-on-year | Liquidity constraints, stock-outs |

| Peloton | Overestimated demand | Inventory build-up during downturn | Cash strain, warehouse backlog |

🚩 Red Flags for Analysts

- DIO increasing faster than revenue growth

- CCC rising despite flat or declining sales

- Borrowings rising in tandem with inventory

- Mismatch between reported margins and cash flow

- Reversals in inventory write-downs

📜 Detective’s Note

The Cash Conversion Cycle is a silent killer — rarely mentioned, often misunderstood. Companies can report healthy profits while quietly bleeding cash into slow inventory. A rising CCC should trigger a deeper dive: look at inventory aging, turnover, and working capital ratios. Sometimes, the biggest red flag isn’t what’s missing — it’s what isn’t moving.

“There is nothing more deceptive than the stillness of a stocked shelf.” — Sherlock Holmes