The Receivables Riddle: When Sales Don’t Convert to Cash

It was a damp evening when Inspector Lestrade brought us a peculiar case from a shipping conglomerate—high revenues, no cash, and an ever-expanding list of unpaid invoices. Holmes leaned in. “This is no ordinary audit, Watson. It’s a search for phantom revenues.”

“Receivables, when inflated, are like counterfeit banknotes: printed with optimism, but rarely redeemed.”

The Illusion of Revenue

Revenue is the headline, but cash is the footnote. Companies often boast about rising sales, yet their cash flow statements tell a more tragic tale. This mismatch is particularly suspicious when accounts receivable balloons far faster than revenue growth.

Real Case Files of Receivables Gone Rogue

| Company | Region | Receivables Spike | Cash Flow from Ops | Forensic Red Flag |

|---|---|---|---|---|

| Wirecard | Germany | €1.4B in ‘third-party’ receivables | Negative | Nonexistent partners |

| Sinoforest | China/Canada | Massive AR from undisclosed buyers | Negative | Fabricated revenue |

| Punj Lloyd | India | Receivables grew 80% in 2 years | Deeply negative | Uncollected project dues |

Forensic Ratios: DSO and AR Turnover

DSO (Days Sales Outstanding) tells us how long it takes to collect cash from customers. A rising DSO is often the first sign of trouble. Combine it with the Accounts Receivable Turnover Ratio to assess collection efficiency.

DSO = (Accounts Receivable / Total Credit Sales) × Number of Days

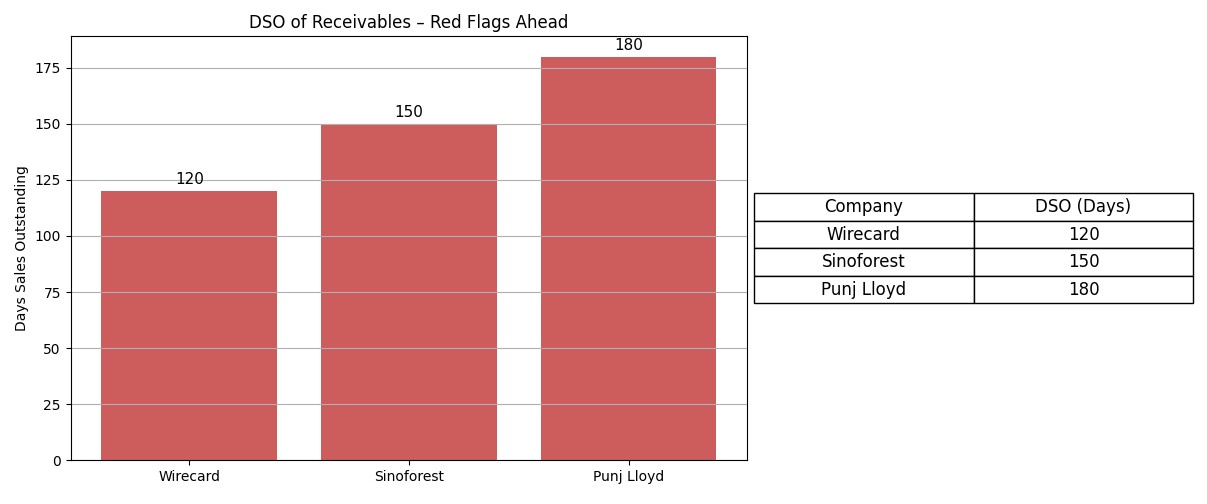

Visual Evidence: DSO Spikes

Below is a chart illustrating DSO trends for three troubled firms:

Common Tricks Behind the Receivables Riddle

| Tactic | What It Looks Like | What’s Really Happening |

|---|---|---|

| Channel Stuffing | Sales spike in Q4 | Distributors overloaded with unsellable stock |

| Fake Invoicing | AR surges, but no delivery | Phantom sales to inflate top-line |

| Slow Collections | Sales look healthy | Customers delaying payments or disputing charges |

Global Cases to Watch

- Steinhoff (South Africa): Overstated receivables hidden across subsidiaries

- DSQ Software (India): Receivables from fake customers to inflate books

- Propping up sales through barter deals or deferred payments disguised as revenue

Detective’s Note 🕵️

- Don’t trust revenue without cash.

- High or rising DSO deserves scrutiny—especially when paired with negative cash flow from operations.

- Always test receivables quality through confirmations, aging analysis, and segment breakdowns.

- Receivables without collection are not assets—they’re clues.

\”There is nothing more deceptive than an obvious fact.\” – Sherlock Holmes